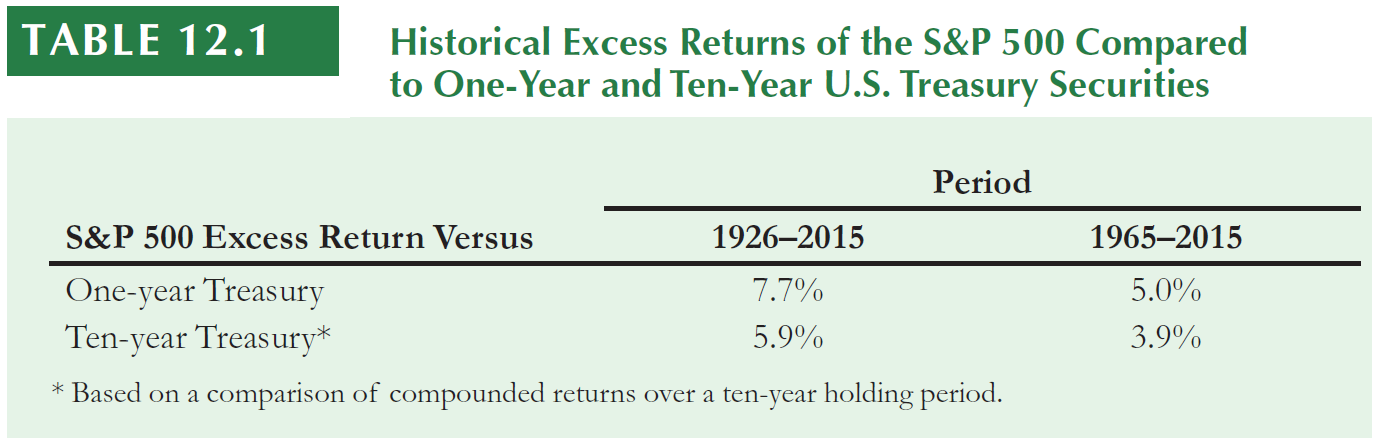

The CAPM Equation for the Cost of Capital (using the Security Market Line).

The cost of capital of any investment opportunity equals the expected return of available investments with the same beta.

\[R_i = R_f + \beta \times (E[R_m] - R_f)\]

12.1 The Equity Cost of Capital

Problem

Suppose you estimate that Disney’s stock (DIS) has a volatility of 20% and a beta of 1.29. A similar process for Chipotle (CMG) yields a volatility of 30% and a beta of 0.55.

Which stock carries more total risk? Which has more market risk?

Disney has more Systematic risk.

Chipotle has more total risk.

12.1 The Equity Cost of Capital

Problem

Suppose you estimate that Disney’s stock (DIS) has a volatility of 20% and a beta of 1.29. A similar process for Chipotle (CMG) yields a volatility of 30% and a beta of 0.55.

If the risk-free interest rate is 3% and you estimate the market’s expected return to be 8%, calculate the equity cost of capital for DIS and CMG. Which company has a higher cost of equity capital?

Because market risk cannot be diversified, it is market risk that determines the cost of capital; thus DIS has a higher cost of equity capital than CMG, even though it is less volatile.

12.1 The Equity Cost of Capital

Suppose you estimate that Walmart’s stock has a volatility of 16.1% and a beta of 0.20. A similar process for Johnson & Johnson yields a volatility of 13.7% and a beta of 0.54. Which stock carries more total risk? Which has more market risk?

Walmart stock has more total risk.

Johnson & Johnson has a higher beta, so it has more market risk

12.1 The Equity Cost of Capital

Suppose you estimate that Walmart’s stock has a volatility of 16.1% and a beta of 0.20. A similar process for Johnson & Johnson yields a volatility of 13.7% and a beta of 0.54. Which stock carries more total risk? Which has more market risk?

If the risk-free interest rate is 4% and you estimate the market’s expected return to be 12%, calculate the equity cost of capital for Walmart and Johnson & Johnson. Which company has a higher cost of equity capital?

\[r_{JNJ}=4\%+0.54×(12\%−4\%)=4\%+4.32\%=8.32\%\]

\[r_{WMT}=4\%+0.20×(12\%−4\%)=4\%+1.6\%=5.6\%\]

Because market risk cannot be diversified, it is market risk that determines the cost of capital; thus, Johnson & Johnson has a higher cost of equity capital than Walmart, even though it is less volatile.

12.2 The Market Portfolio

12.2 The Market Portfolio

To use the CAPM, we need to understand what the market portfolio is.

Because the market portfolio is the total supply of securities, the proportions of each security should correspond to the proportion of the total market that each security represents.

Thus, the market portfolio contains more of the largest stocks and less of the smallest stocks.

Market capitalization (of one firm):

The total market value of a firm’s outstanding shares

\(\epsilon_i\) is the error term or the residual. It represents the deviation from the best-fitting line and is zero on average (or else we could improve the fit). This error term corresponds to the diversifiable risk of the stock, which is the risk that is uncorrelated with the market.

12.3 Beta Estimation

\(\alpha_i\) is the constant term. It measures the historical performance of the security relative to the expected return predicted by the security market line.

It is the distance that the stock’s average return is above or below the SML. Thus, we can say \(\alpha_i\) is a risk-adjusted measure of the stock’s historical performance.

According to the CAPM, \(\alpha_i\) should not be significantly different from zero.

12.3 Beta Estimation

Finally, we can estimate Beta using the formula (use market s.d. = 10%):

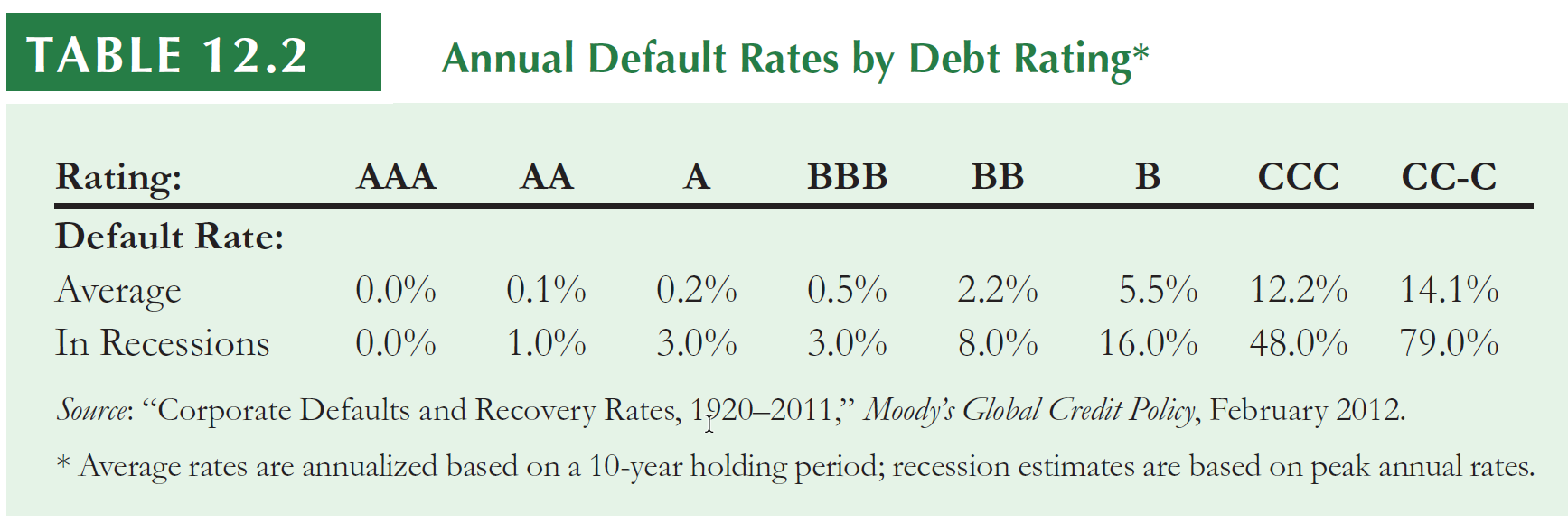

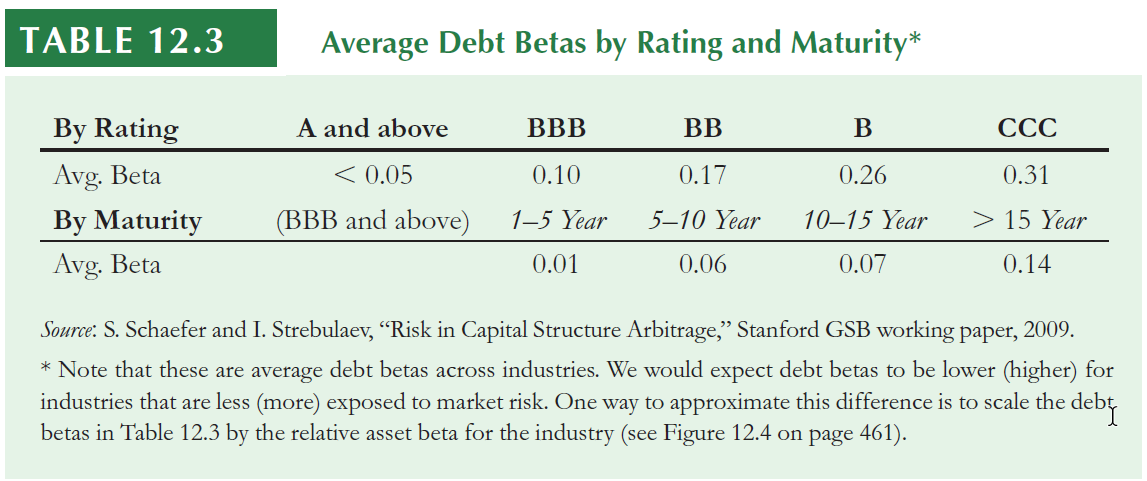

Debt betas are difficult to estimate because corporate bonds are traded infrequently.

One approximation is to use estimates of betas of bond indices by rating category.

12.4 The Debt Cost of Capital

12.4 The Debt Cost of Capital

Problem

In early 2013, auto parts retailer Autozone had outstanding 10-year bonds with a yield to maturity of 3% and a BBB rating. If corresponding risk-free rates were 1.5% and the market risk premium is 8%, estimate the expected return of Autozone’s debt.

Solution I

Using the average estimates in Table 12.2 and an expected loss rate of 60%, from Eq. 12.7 we have

\[R_d = 3\% - 0.5\% \times 0.6 = 2.7\%\]

Solution II

Alternatively, we can estimate the bond’s expected return using CAPM and an estimated beta of 0.10 from Table 12.3.

In that case, \(R_d = 1.5\% + 0.10(8\%) = 2.3\%\).

12.4 The Debt Cost of Capital

Both estimates are rough approximations and they both suggest that the expected return of Autozone’s debt is below its yield-to-maturity of 3%.

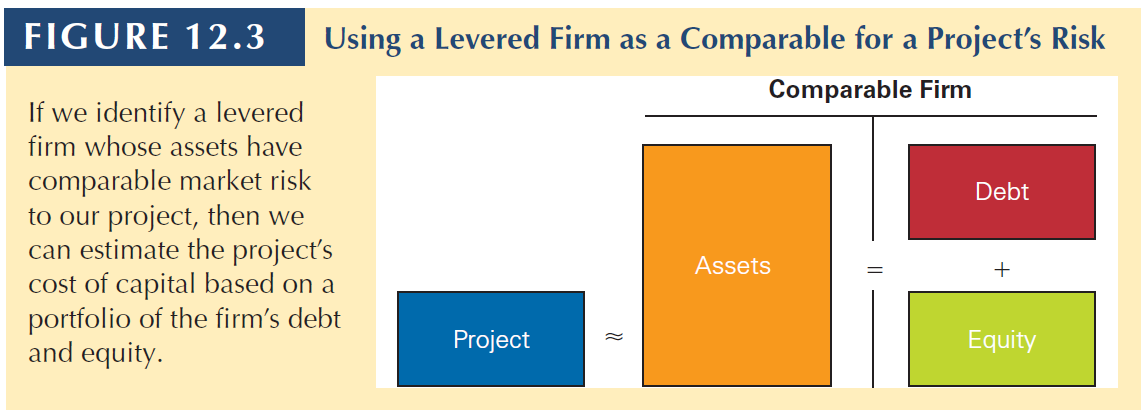

12.5 A Project’s Cost of Capital

12.5 A Project’s Cost of Capital

We want now to estimate the cost of capital of a project.

Because a new project is not itself a publicly traded security, we cannot use historical risks of equity and debt to estimate beta and the cost of capital.

Also, the decision to invest in projects using the firm’s cost of capital might ignore the project’s risk.

12.5 A Project’s Cost of Capital

12.5 A Project’s Cost of Capital

Instead, the most common method for estimating a project’s beta is to identify comparable firms in the same line of business as the project we are considering undertaking.

All-Equity Comparables

The simplest setting of a theoretical comparable firm is to find an all-equity financed firm (a firm with no debt) in a single line of business that is comparable to the project.

Then, use the comparable firm’s equity beta and cost of capital as estimates.

The main idea here is that your project is an asset, so if you find an all-equity firm, the equity beta will also be the beta of its assets. Thus, you can use this estimate as the beta of your project.

Remember that:

Assets = Equity + Debt.

When debt is zero: Assets = Equity.

12.5 A Project’s Cost of Capital

Equity beta: the one we measured before.

Asset beta: it is the beta of all assets in a firm, which is the same beta of the combination of Equity + Debt.

Debt beta: the changes in the expected return by 1% change in the market returns.

If your project is comparable to the assets of a firm, you can use its beta as your project’s beta.

But again, the firm might be all-equity or might have debt.

12.5 A Project’s Cost of Capital

Estimating the Beta of a Project from a Single-Product Firm

Problem

You have just invented a new low-cost, long-lasting rechargeable battery for use in electric cars.

You are working on your business plan, and believe your firm will face similar market risk to Seguin Inc, which has a beta of 1.3.

To develop your financial plan, estimate the cost of capital of financing your firm assuming a risk-free rate of 2.5% and a market risk premium of 6.5%.

Using Seguin’s beta as the estimate of the project beta (i.e., assuming the market risk of your project is the same as this company’s):

Your firm is launching a new product and you identify Company X as a firm with comparable investments.

X’s equity has a market capitalization of 77 billion and a beta of 0.75. X also has 57 billion of AA-rated debt outstanding, with an average yield of 4.1%.

Estimate the cost of capital of your firm’s investment given a risk-free rate of 2.5% and a market risk-premium of 6%.

Company’s X equity cost of capital is:

\[ R_e = 2.5\% + 0.75 \times 6\% = 7\%\]

Company’s X unlevered cost of capital is (using the yield as debt cost):

Apple’s market capitalization in mid-2016 was $484 billion, and its beta was 1.03. At that same time, the company had $25 billion in cash and $69 billion in debt. Based on this data, estimate the beta of Apple’s underlying business enterprise.

Note that the firm is less risky than its equity portion due to its cash holdings.

12.5 A Project’s Cost of Capital

Industry Betas

Remember that estimating the beta of a stock only contains estimation error.

Instead, you can estimate the beta of a whole industry to reduce the estimate error.

12.6 Project Risk and Financing

12.6 Project Risk and Financing

In this final section, we want to account for risk differences between projects.

Individual projects may be more or less sensitive to market risk.

One important thing is that:

firm asset betas reflect the market risk of the average project in the firm.

But individually, projects can differ in risk.

For instance, think about a multi-divisional firm.

Each division will likely have its own level of market risk.

12.6 Project Risk and Financing

Operating leverage

Additionally, operating leverage can also affect the project’s risk.

High operating leverage, high risk.

Operating leverage is the proportion of fixed costs over total costs.

A higher proportion of fixed costs increases the sensitivity of the project’s cash flows to market risk.

The project’s beta will be higher

A higher cost of capital should be assigned

12.6 Project Risk and Financing

Now, we have all that is necessary to compute the Weighted Average Cost of Capital (WACC).

Assuming the existence of Taxes:

\[R_{wacc} = \frac{E}{D+E}\times R_e + \frac{D}{D+E} \times R_d \times (1-\phi_c)\] This is the after-tax WACC.

Because interest expense is tax deductible, the WACC is less than the expected return of the firm’s assets. Meaning, you do not pay taxes on debt interests, which makes the after-tax WACC decrease in comparison to the pre-tax WACC

CAPM is very practical and straightforward to implement, the CAPM-based approach is very robust

CAPM imposes a disciplined process on managers to identify the cost of capital.

CAPM make the capital budgeting process less subject to managerial manipulation than if managers could set project costs of capital without clear justification.

CAPM is often the model many investors use to evaluate risk.

CAPM gets managers to think about risk in the correct way. That is, to think about market risk, instead of total risk.