Event studies measure the impact of a specific event on stock returns.

Widely used in empirical finance:

Earnings announcements

Mergers and acquisitions

SEOs/IPOs

Credit rating downgrades

Regulatory changes

“Using financial market data, an event study measures the impact of a specific event on the value of a firm.” (MacKinlay, 1997)

Introduction

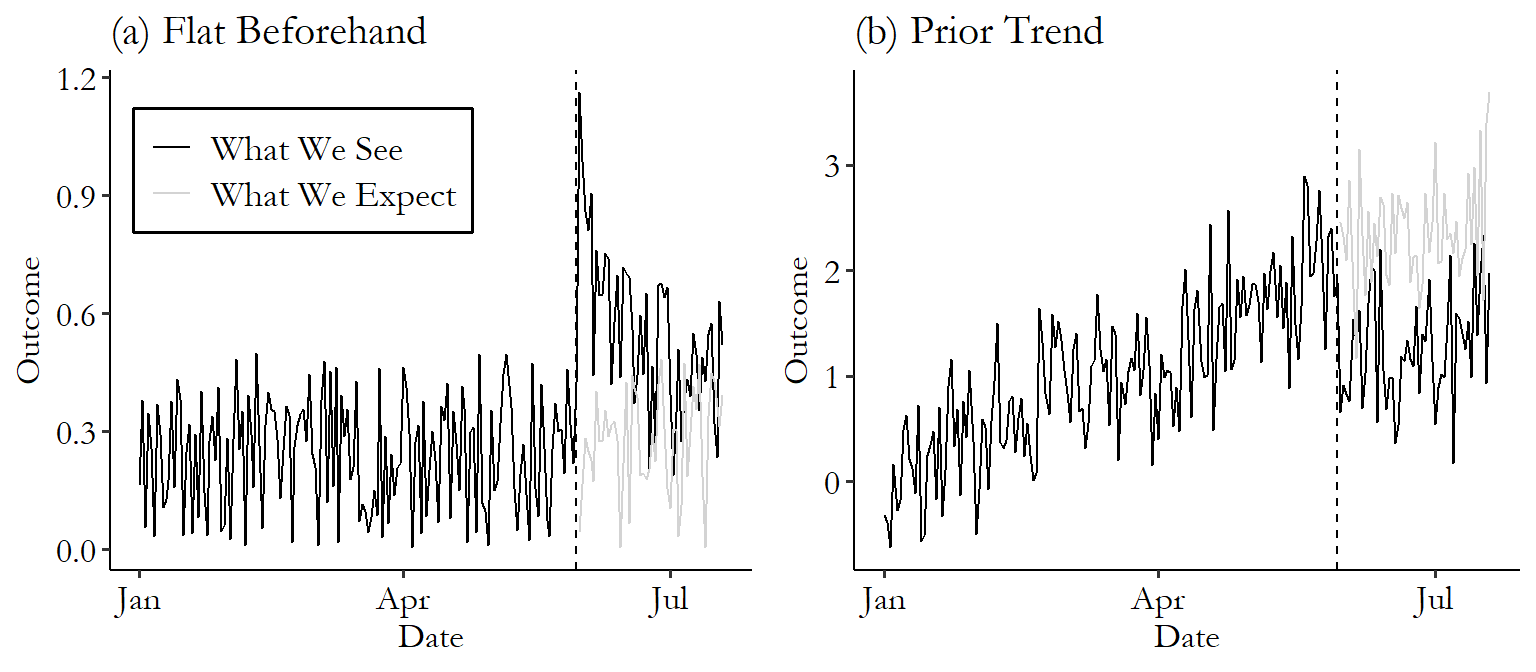

The event study is probably the oldest and simplest causal inference research design.

It predates experiments. It predates statistics. It probably predates human language. It might predate humans.

The idea is this: at a certain time, an event occured, leading a treatment to be put into place at that time. Whatever changed from before the event to after is the effect of that treatment.

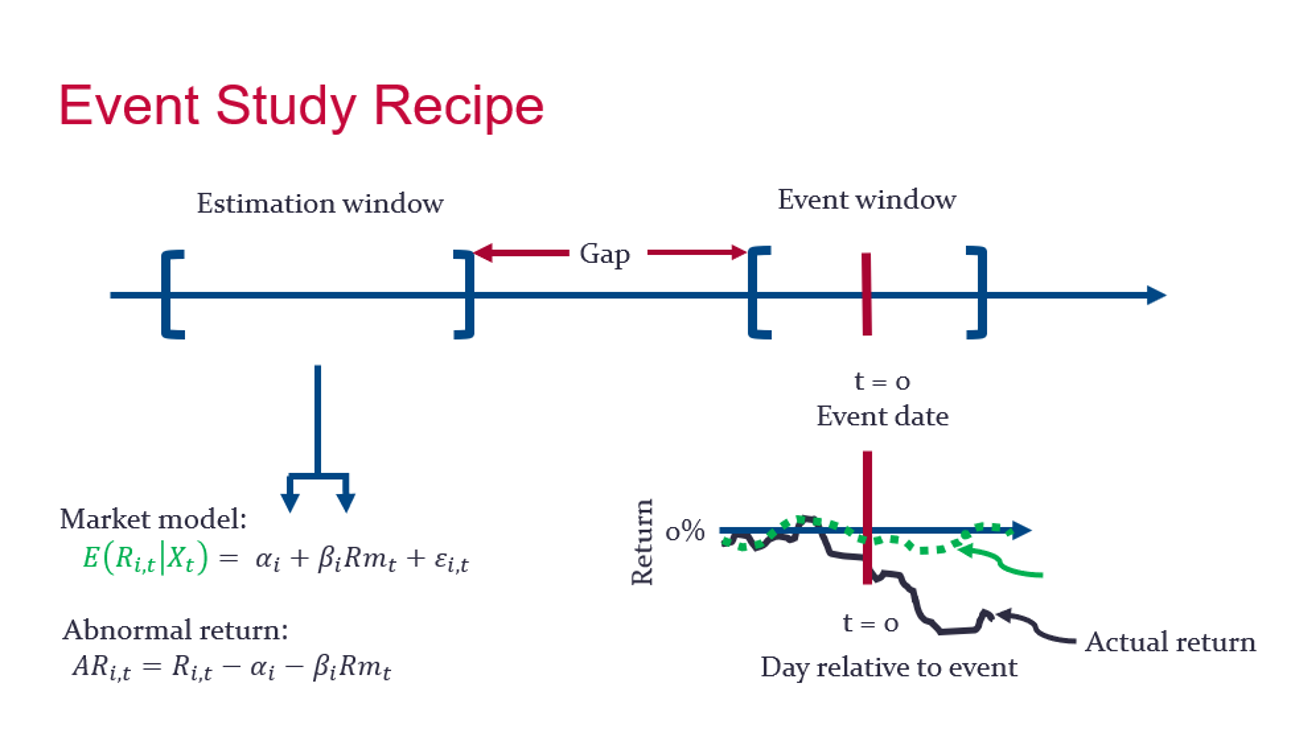

The process for doing one of these event studies is as follows:

Pick an “estimation period” a fair bit before the event, and an “observation period” from just before the event to the period of interest after the event.

Use the data from the estimation period to estimate a model that can make a prediction of the stock’s return in each period. A popular way of doing this are:

Risk-adjusted returns model. Use the data from the estimation period to fit a regression describing how related the return is to other market portfolios, like the market return: \(R=\alpha + \beta \times R_m\). Then, in the observation period, use that model and the actual to predict in each period.

In the observation period, subtract the prediction from the actual return to get the “abnormal return.”

\(AR = R - \hat{R}\)

Look at \(AR\) in the observation period. Nonzero values before the event imply the event was anticipated, and nonzero values after the event give the effect of the event on the stock’s return.

Introduction

Methodology

Steps of an Event Study

The central idea: measure abnormal returns (AR).

\[AR_{it} = R_{it} - E[R_{it}|X_t]\]

Define event date (day 0).

Select event window (e.g., [-1,+1], [-5,+5]).

Select estimation window (e.g., -120 to -20 days).

A positive CAR suggests good news (value creation).

A negative CAR suggests bad news (value destruction).

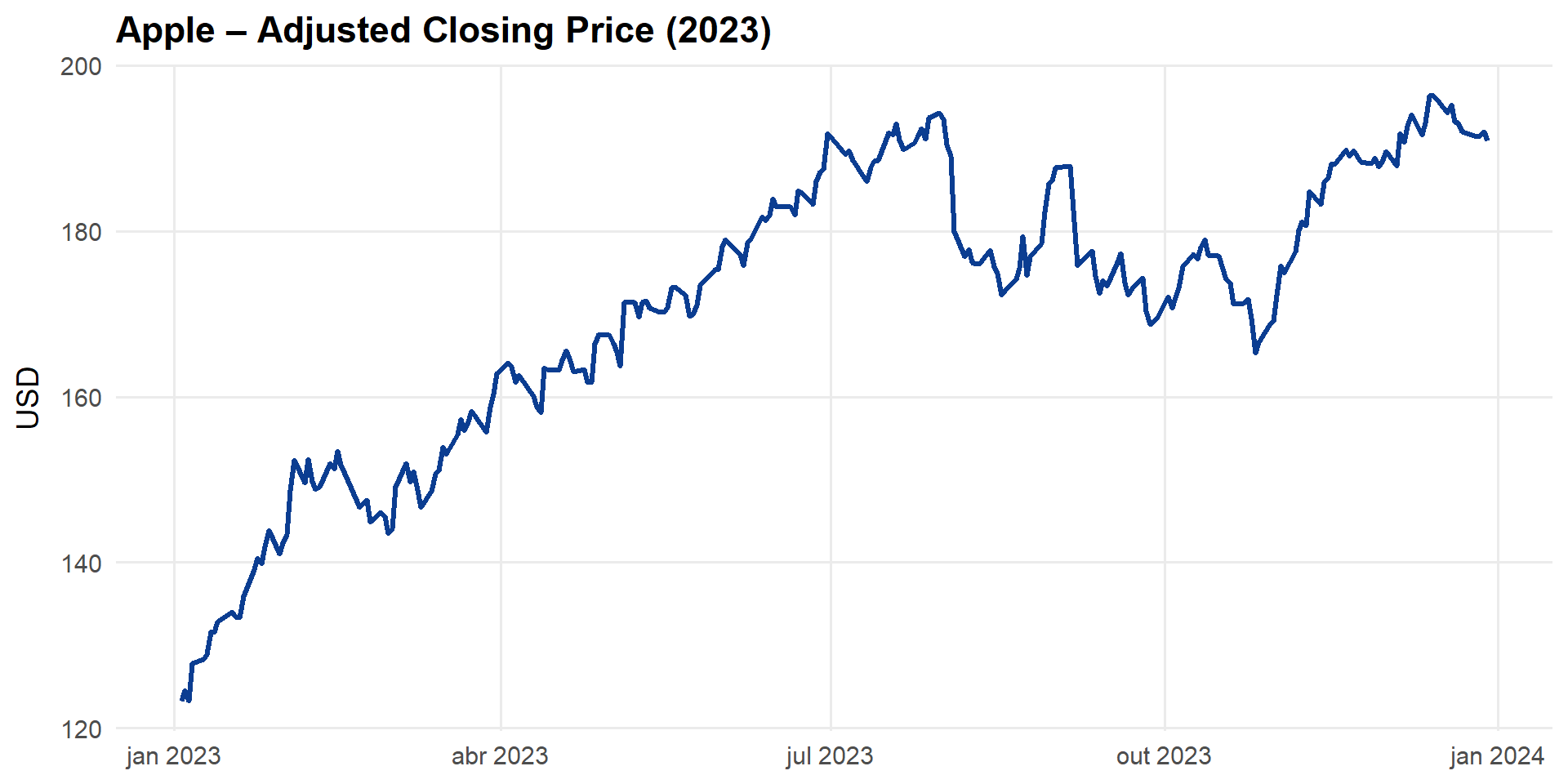

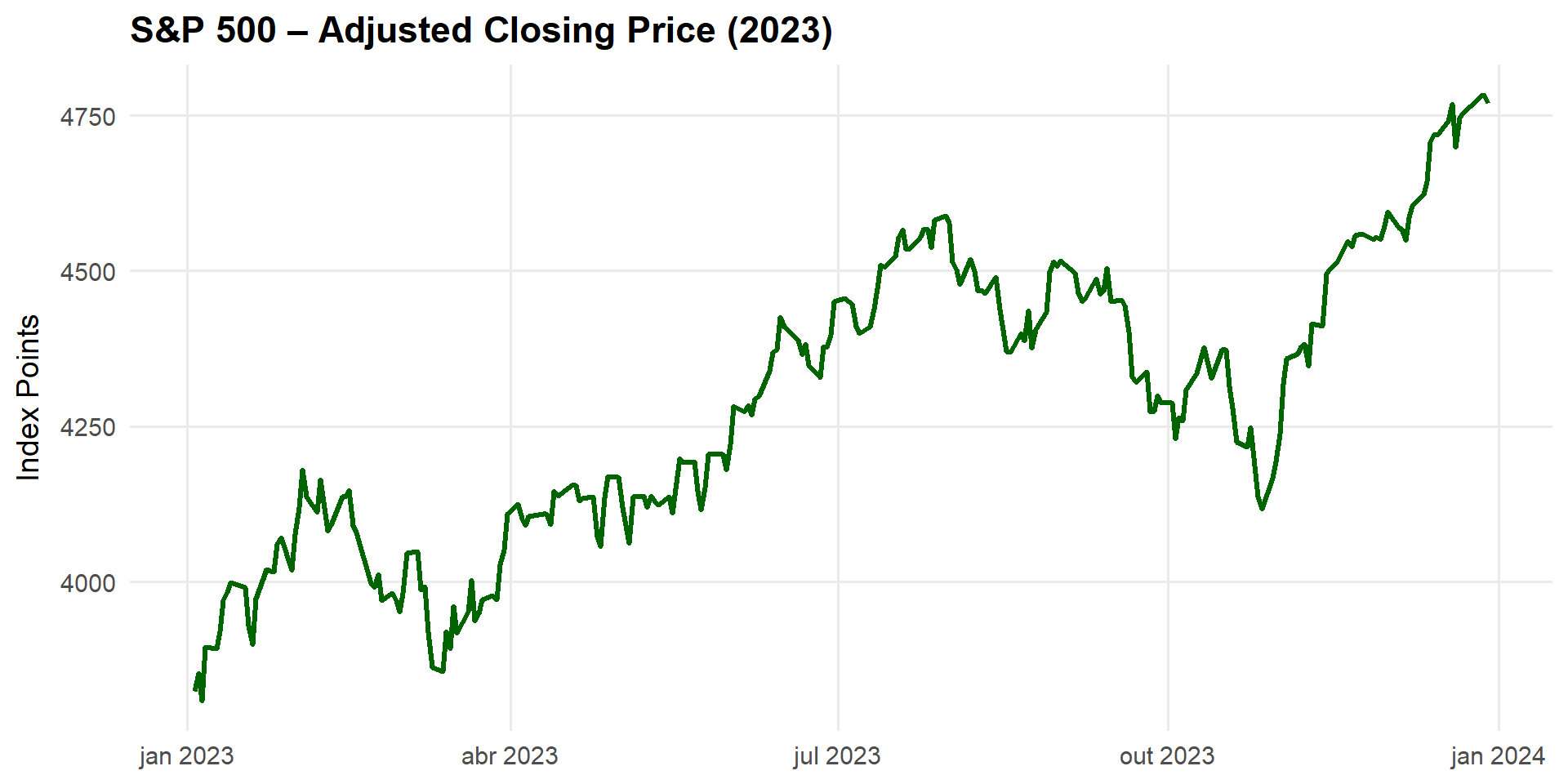

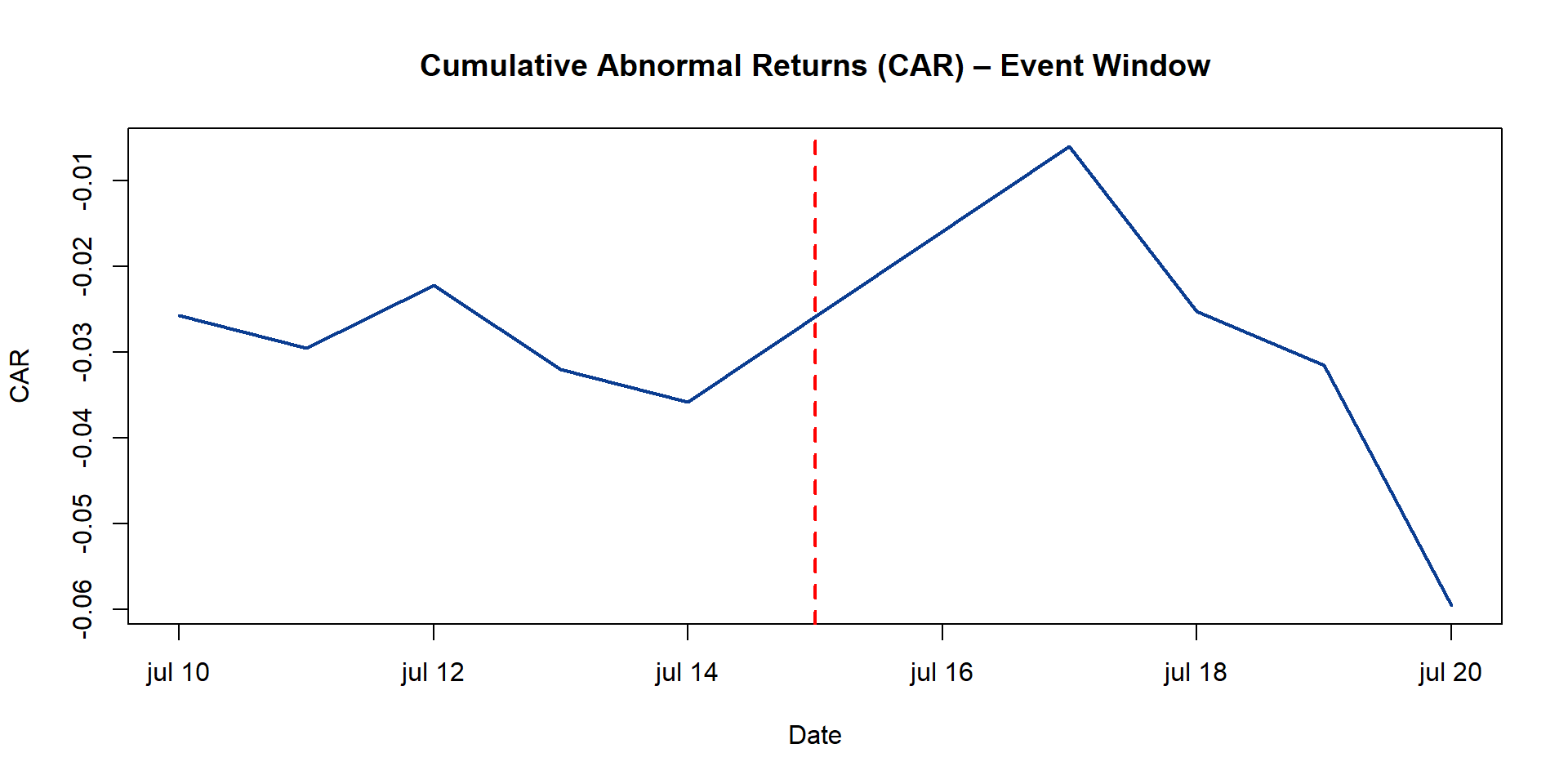

Step 4 – Visualize CAR

Code

# Extract abnormal returns only for the event windowar_window <- ar[window]# Recalculate CAR starting at 0car <-cumsum(as.numeric(ar_window))# Plot corrected CARplot(index(ar_window), car, type ="l", col ="#0b3d91", lwd =2,main ="Cumulative Abnormal Returns (CAR) – Event Window",xlab ="Date", ylab ="CAR")abline(v = event_date, col ="red", lwd =2, lty =2)

What is the CAR in this window?

Estimation window: 120 trading days before the event (used to estimate the market model).

Event window: [-5, +5] days around the event date (used to measure the abnormal impact).

The CAR (Cumulative Abnormal Return) is the sum of abnormal returns across this event window.

Code

ar_window <- ar[window] # abnormal returns in the event window [-5,+5]car <-cumsum(as.numeric(ar_window)) # cumulative abnormal returns, starting at 0CAR_total <-last(car) # CAR over the full event windowCAR_total

[1] -0.05950583

Robustness table

CAR robustness across estimation and event windows

est_window_days

event_window

n_est

n_event

alpha_hat

beta_hat

CAR

t_CAR

60

[-10,+10]

41

15

0.00073

0.862

-0.0260

-0.95

60

[-3,+3]

41

5

0.00073

0.862

0.0039

0.22

60

[-5,+5]

41

9

0.00073

0.862

-0.0198

-0.81

120

[-10,+10]

82

15

0.00077

1.102

-0.0327

-1.14

120

[-3,+3]

82

5

0.00077

1.102

-0.0025

-0.13

120

[-5,+5]

82

9

0.00077

1.102

-0.0276

-1.10

180

[-10,+10]

124

15

0.00181

1.098

-0.0481

-1.68

180

[-3,+3]

124

5

0.00181

1.098

-0.0076

-0.40

180

[-5,+5]

124

9

0.00181

1.098

-0.0367

-1.47

Extensions

Extensions and Practical Challenges

Multiple events

Often researchers examine a wave of events (e.g., several M&As in one industry, multiple SEOs).

Challenge: heterogeneity across firms and event timing. Aggregation must be justified.

Extensions and Practical Challenges

Clustering of events

Many events occur on the same date (e.g., quarterly earnings announcements).

Standard errors may be underestimated if cross-sectional dependence is ignored.

Solutions: event-time portfolios, clustered or robust standard errors.

Extensions and Practical Challenges

Confounding events

Other major news may coincide with the focal event (e.g., macro policy change).

Makes it difficult to attribute abnormal returns exclusively to the event of interest.

Extensions and Practical Challenges

Long-horizon event studies

Extending the event window to months/years raises econometric issues.

CARs accumulate model error and are sensitive to the choice of expected-return model.

Interpretation becomes less about short-term information effects, more about long-run performance.