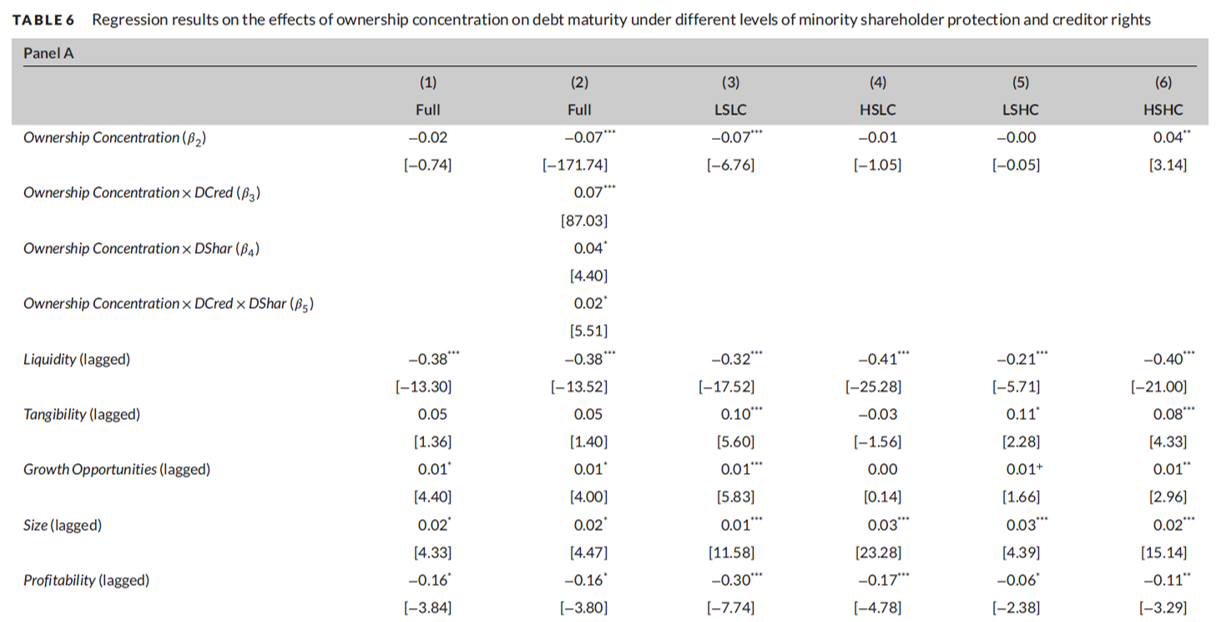

Empirical Methods in Finance

Part 1

Você nunca sabe o resultado do caminho que não toma.

Como fazemos na prática?

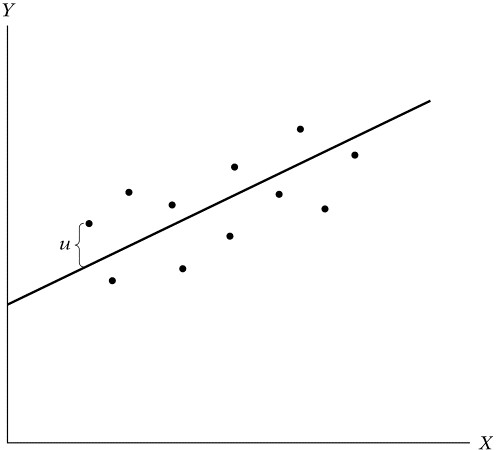

Exemplo de modelo empírico:

\(Y_{i} = α + 𝜷_{1} × X_i + Controls + error\)

Uma vez que estimemos esse modelo, temos o valor, o sinal e a significância do \(𝜷\).

Se o Beta for significativamente diferente de zero e positivo –> X e Y estão positivamente correlacionados.

O problema? Os pacotes estatísticos que utilizamos sempre “cospem” um beta. Seja ele com ou sem viés.

Cabe ao pesquisador ter um design empírico que garanta que o beta estimado tenha validade interna.

Como fazemos na prática?

A decisão final é baseada na significância do Beta estimado. Se significativo, as variáveis são relacionadas e fazemos inferências em cima disso.

Contudo, sem um design empírico inteligente, o beta encontrado pode ter literalmente qualquer sinal e significância.

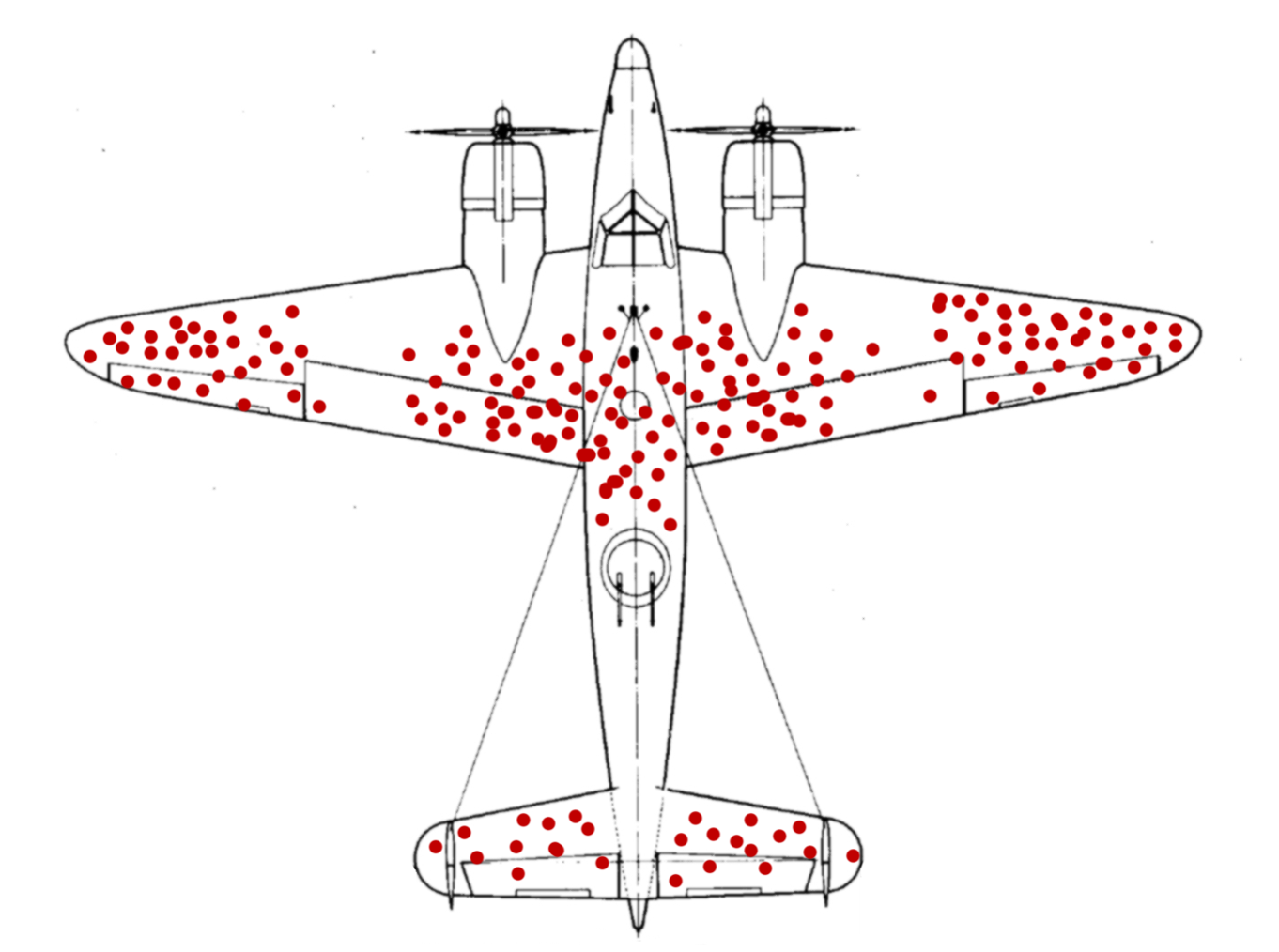

Exemplo desses problemas

Veja esse site.

Exemplo desses problemas

Veja esse site.

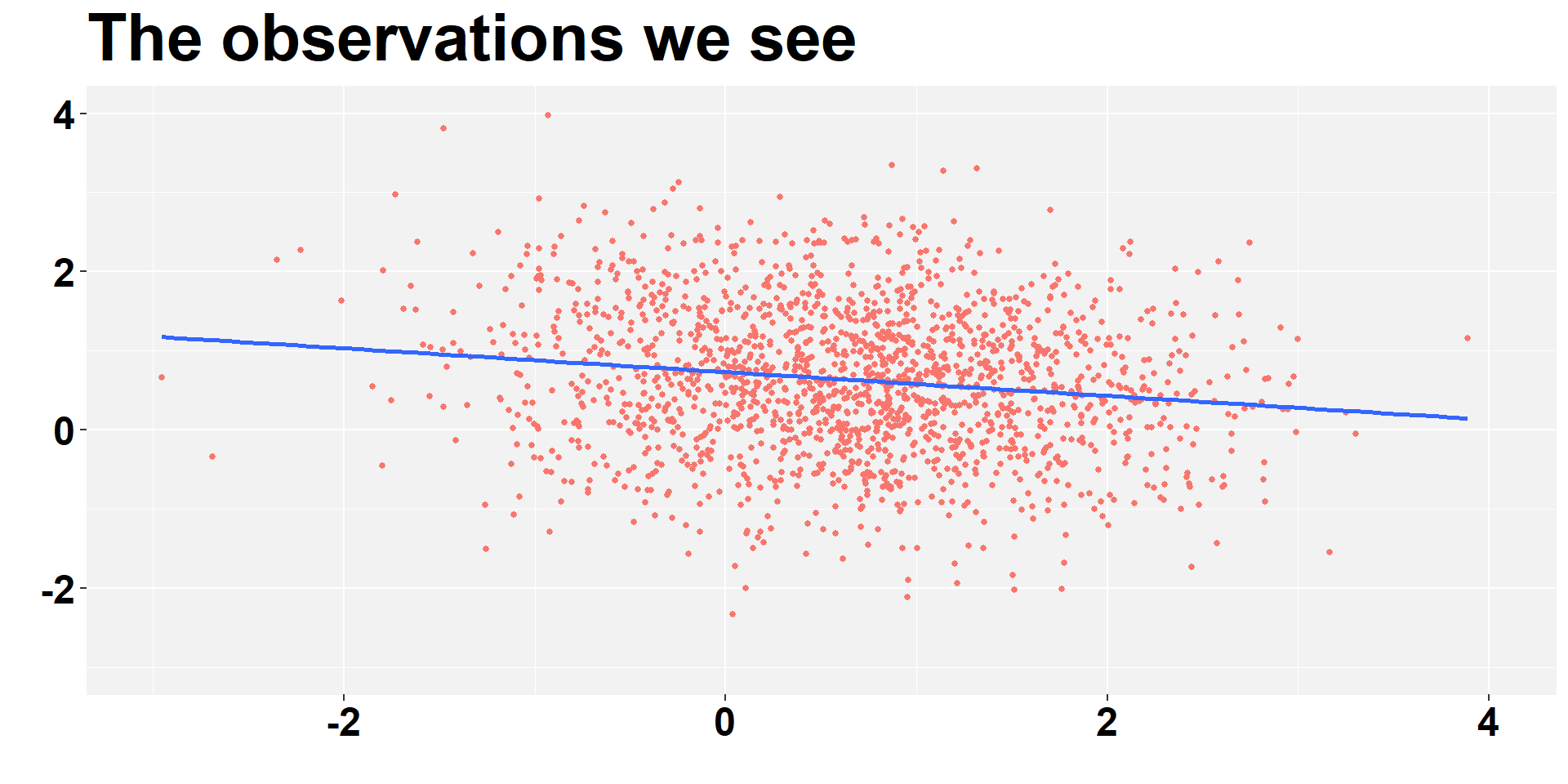

Selection bias - We see I

R

library(data.table)

library(ggplot2)

# Generate Data

n = 10000

set.seed(100)

x <- rnorm(n)

y <- rnorm(n)

data1 <- 1/(1+exp( 2 - x - y))

group <- rbinom(n, 1, data1)

# Data Together

data_we_see <- subset(data.table(x, y, group), group==1)

data_all <- data.table(x, y, group)

# Graphs

ggplot(data_we_see, aes(x = x, y = y)) +

geom_point(aes(colour = factor(-group)), size = 1) +

geom_smooth(method=lm, se=FALSE, fullrange=FALSE)+

labs( y = "", x="", title = "The observations we see")+

xlim(-3,4)+ ylim(-3,4)+

theme(plot.title = element_text(color="black", size=30, face="bold"),

panel.background = element_rect(fill = "grey95", colour = "grey95"),

axis.text.y = element_text(face="bold", color="black", size = 18),

axis.text.x = element_text(face="bold", color="black", size = 18),

legend.position = "none")

Python

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

n = 10000

np.random.seed(100)

x = np.random.normal(size=n)

y = np.random.normal(size=n)

data1 = 1 / (1 + np.exp(2 - x - y))

group = np.random.binomial(1, data1, n)

data_we_see = pd.DataFrame({'x': x[group == 1], 'y': y[group == 1], 'group': group[group == 1]})

data_all = pd.DataFrame({'x': x, 'y': y, 'group': group})

sns.set(style='whitegrid')

plt.figure(figsize=(7, 5))

plt.scatter(data_we_see['x'], data_we_see['y'], c=-data_we_see['group'], cmap='viridis', s=20)

sns.regplot(x='x', y='y', data=data_we_see, scatter=False, ci=None, line_kws={'color': 'blue'})

plt.title("The observations we see", fontsize=18)

plt.xlabel("")

plt.ylabel("")

plt.show()

Stata

clear all

set seed 100

set obs 10000

gen x = rnormal(0,1)

gen y = rnormal(0,1)

gen data1 = 1 / (1 + exp(2 - x - y))

gen group = rbinomial(1, data1)

twoway (scatter x y if group == 1, mcolor(black) msize(small)) (lfit y x if group == 1, color(blue)),title("The observations we see", size(large) ) xtitle("") ytitle("")

quietly graph export figs/graph1.svg, replace

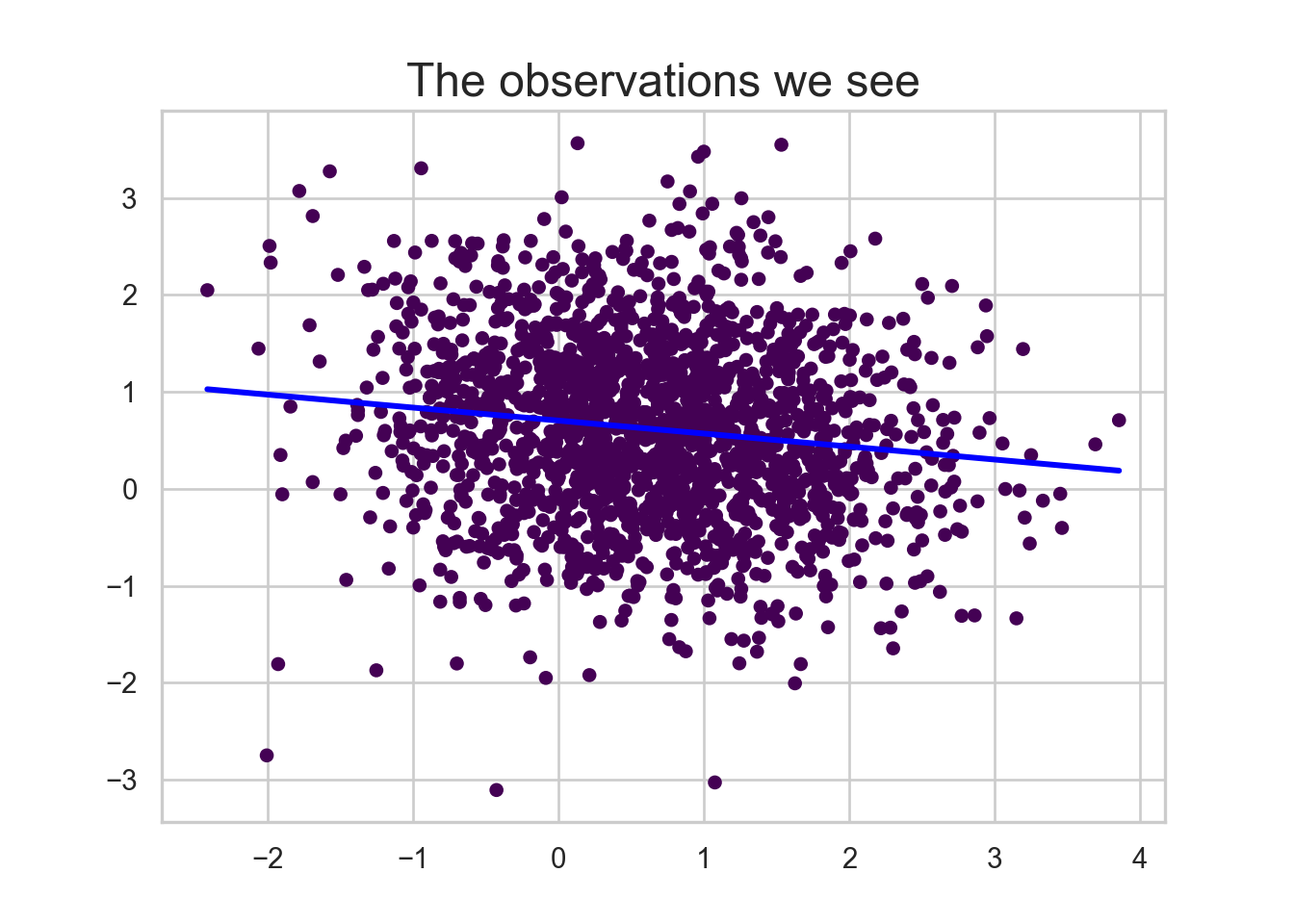

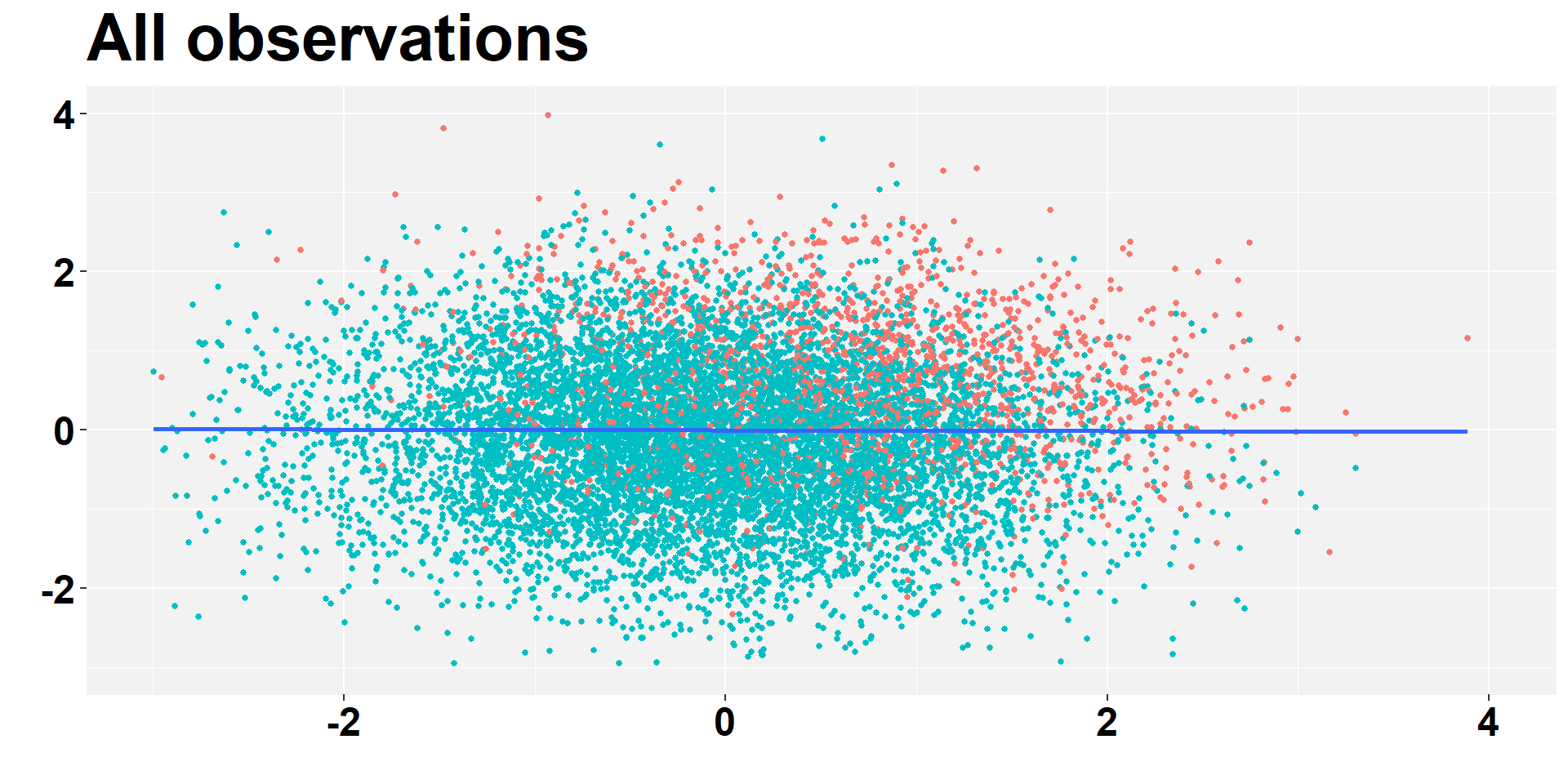

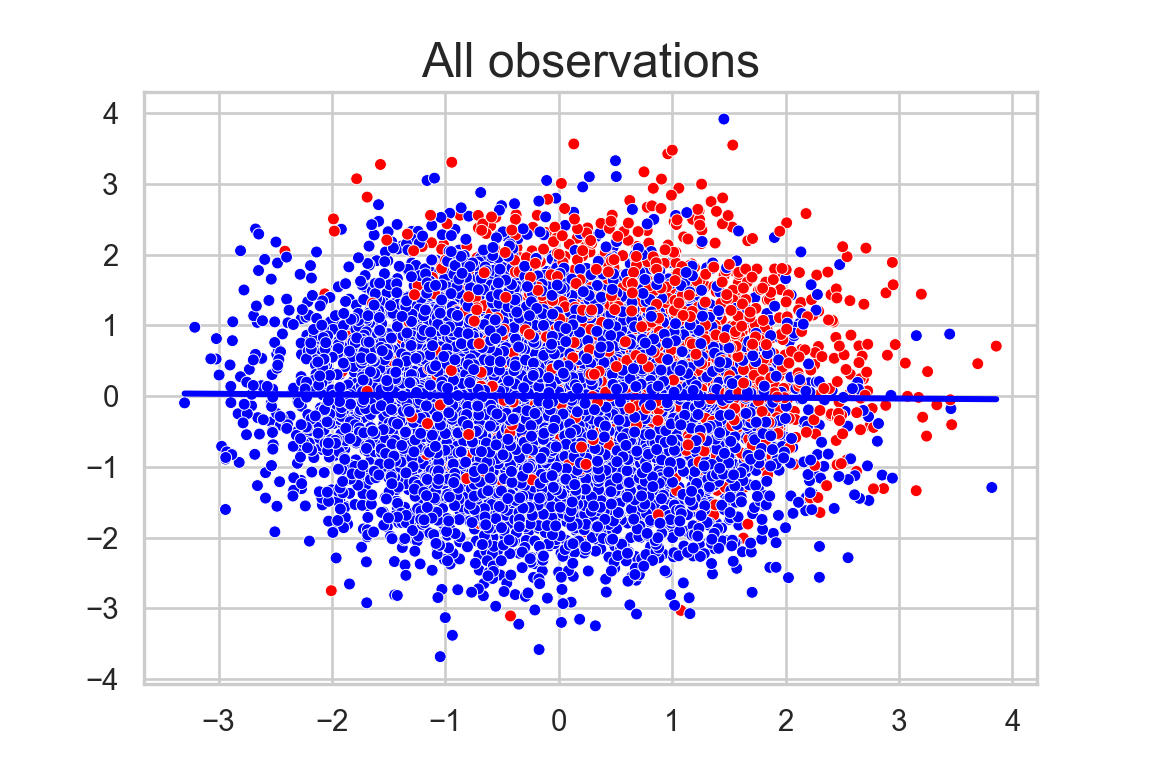

Selection bias - All I

R

ggplot(data_all, aes(x = x, y = y, colour=group)) +

geom_point(aes(colour = factor(-group)), size = 1) +

geom_smooth(method=lm, se=FALSE, fullrange=FALSE)+

labs( y = "", x="", title = "All observations")+

xlim(-3,4)+ ylim(-3,4)+

theme(plot.title = element_text(color="black", size=30, face="bold"),

panel.background = element_rect(fill = "grey95", colour = "grey95"),

axis.text.y = element_text(face="bold", color="black", size = 18),

axis.text.x = element_text(face="bold", color="black", size = 18),

legend.position = "none")

Python

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

sns.set(style='whitegrid')

plt.figure(figsize=(6, 4))

sns.scatterplot(data=data_all, x='x', y='y', hue='group', palette=['blue', 'red'], s=20)

sns.regplot(data=data_all, x='x', y='y', scatter=False, ci=None, line_kws={'color': 'blue'})

plt.title("All observations", fontsize=18)

plt.xlabel("")

plt.ylabel("")

plt.legend(title="Group", labels=["0", "1"], loc="upper left")

plt.gca().get_legend().remove()

plt.show()

Number of observations (_N) was 0, now 10,000.

Exemplo desses problemas

Source: Angrist

Não podemos pegar dois caminhos.

Exemplo desses problemas

Source: Angrist

Não podemos comparar pessoas que não são comparáveis.

🙋♂️ Any Questions?

Thank You!