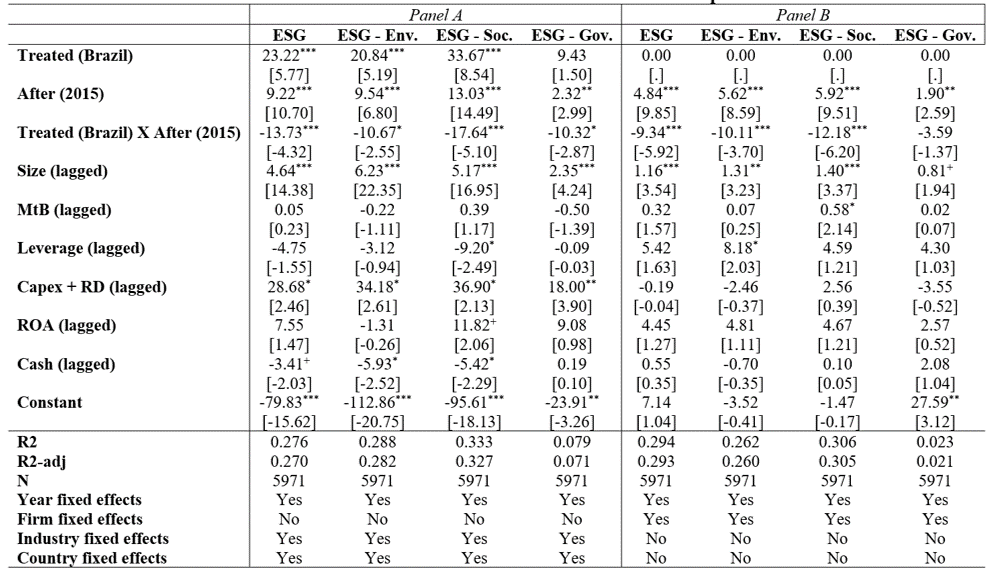

Models

Model 1:

\(ESG_{i,t} = β_1 + β_2 × Competition_{i,t-1} + β_3 × Size_{i,t-1} + β_4 × MtB_{i,t-1} + \\ β_5 × Leverage_{i,t-1} + β_6 × Capex + RD_{i,t-1} + β_7 × ROA_{i,t-1} + \\ β_8 × Cash_{i,t-1} + ϕ_{time} + ϵ_{i,t}\)

Model 2:

\(ESG_{i,t} = β_1 + β_2 × Treated (Brazil) + β_3 × After (2015) + \\ β_4×Treated (Brazil) × After (2015) + β_5 × Size_{i,t-1} + β_6 × MtB_{i,t-1} + \\ β_7 × Leverage_{i,t-1} + β_8 × Capex + RD_{i,t-1} + β_9 × ROA_{i,t-1} + \\ β_{10} × Cash_{i,t-1} + ϕ_{time} + ϵ_{i,t}\)

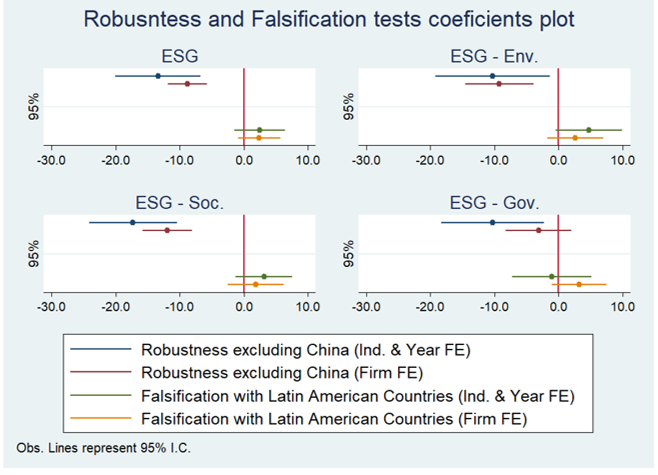

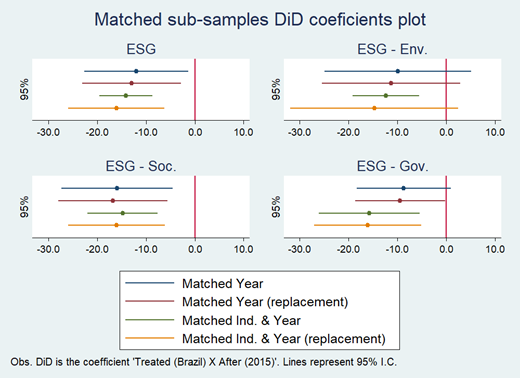

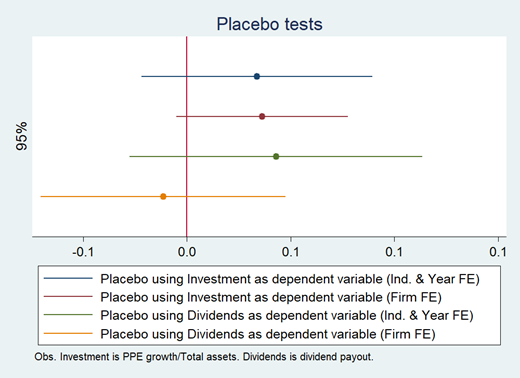

Main Results (Robustness and Falsification)

Robustness: Excluding China

Falsification: “Shock” in Latin America Countries, instead of Brazil