Inferência Causal em Pesquisas de Finanças: Problemas e Soluções

Enanpad 2024

17-09-2024

The challenge

- I will discuss some issues in using plain OLS models in Finance Research (mainly with panel data).

I will avoid the word “endogeneity” as much as possible.

- This word refers to the violation of the Conditional Mean Independence (CMI) assumption, meaning that \(x\) and \(\mu\) are correlated.

- I will also avoid the word “identification” because identification does not guarantee causality and vice-versa (Kahn and Whited 2017)

- The discussion is mainly based on Atanasov and Black (2016)

The challenge

Imagine that you want to investigate the effect of Governance on Q

- You may have more covariates explaining Q (omitted from slides)

\(𝑸_{i} = α + 𝜷 × Gov_{i} + Controls + error\)

All the issues in the next slides will make it not possible to infer that changing Gov will CAUSE a change in Q

That is, cannot infer causality

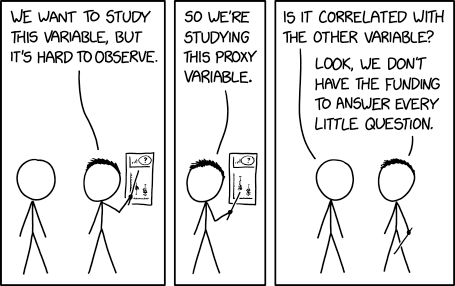

8) Construct validity

Some constructs (e.g. \(Gov\)) are complex and sometimes have conflicting mechanisms.

We usually don’t know for sure what “good” governance is, for instance.

It is common to use imperfect proxies, that may poorly fit the underlying concept.

13) Self-Selection

Self-selection is a type of selection bias. Usually, firms decide which level of governance they adopt

It is like they “self-select” into the treatment.

- Units decide whether they receive the treatment or not

There are reasons why firms adopt high governance

- If observable, you need to control for. If unobservable, you have a problem.

Important

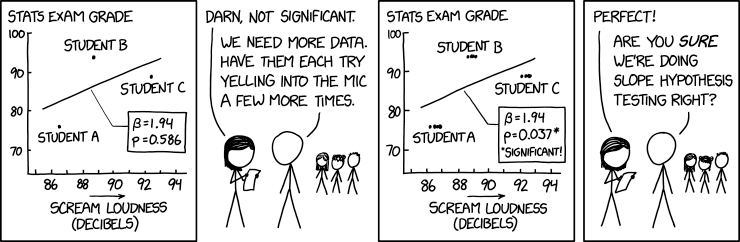

More data is not necessarily a solution, you need a sound empirical design.

THANK YOU!

QUESTIONS?

Henrique C. Martins